Crypto TDS in India has significantly changed how cryptocurrency transactions are taxed in 2025. With the introduction of a 1% TDS on crypto transactions under Section 194S, investors and traders must understand how this rule works to stay compliant and avoid penalties. Whether you trade Bitcoin, Ethereum, or other cryptocurrencies, this guide explains everything about the 1% crypto TDS rule in India, including who must deduct it, how it is calculated, and how it impacts your overall crypto tax liability.

What Is Crypto TDS in India?

Crypto TDS (Tax Deducted at Source) is a mechanism introduced by the Indian government to track cryptocurrency transactions and ensure tax compliance.

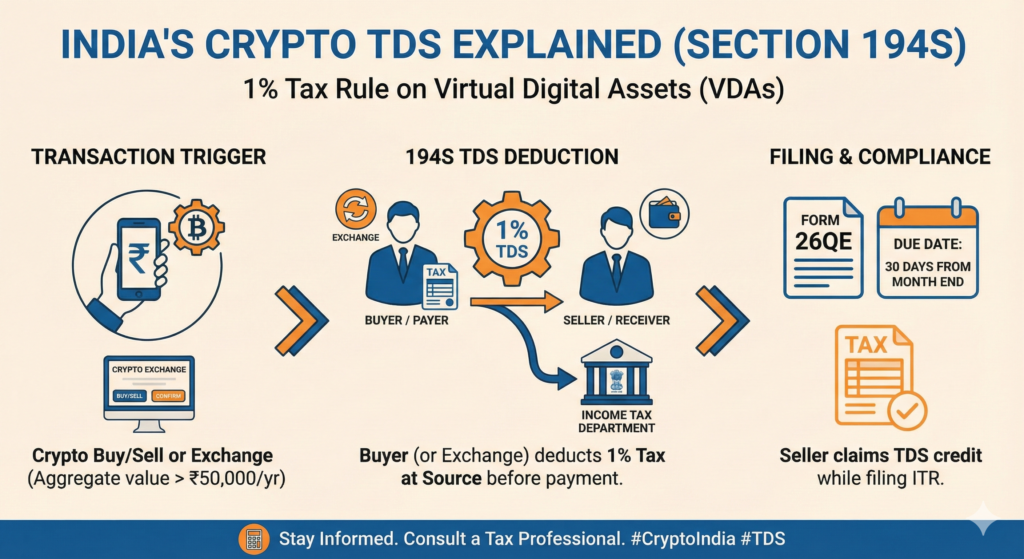

Under Section 194S of the Income Tax Act, a 1% TDS is applicable on the transfer of Virtual Digital Assets (VDAs) such as cryptocurrencies and NFTs. This rule applies regardless of whether the transaction results in profit or loss.

What Is the 1% Crypto TDS Rule?

The 1% crypto TDS rule means that 1% of the transaction value is deducted at the time of buying or selling crypto. It is not a tax on profit but a deduction on the gross transaction amount.

Key points:

- Flat 1% rate

- Applies per transaction

- Deducted at source

- Adjustable against final tax liability

When Does 1% TDS Apply to Crypto Transactions?

Crypto TDS applies in the following cases:

- Buying cryptocurrency

- Selling cryptocurrency

- Trading crypto on exchanges

- Peer-to-peer (P2P) crypto transactions

- Payments made using cryptocurrency

Even if you incur a loss, crypto TDS in India still applies.

Who Is Responsible for Deducting Crypto TDS?

Responsibility depends on the transaction type:

1. Crypto Exchanges

If you trade on Indian crypto exchanges, the exchange deducts TDS automatically.

2. Peer-to-Peer (P2P) Transactions

In P2P trades, the buyer is responsible for deducting and depositing TDS.

Failure to deduct TDS in P2P transactions can attract penalties.

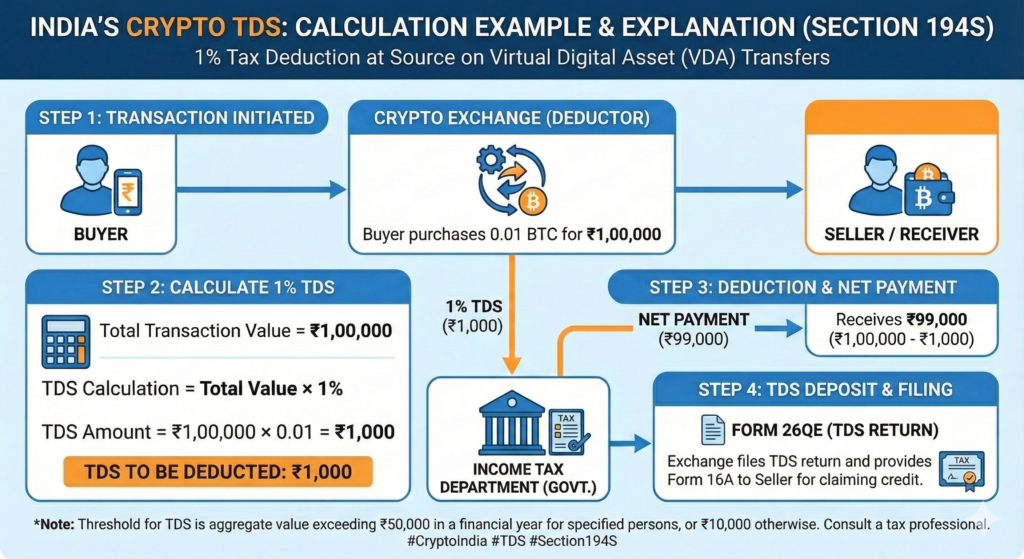

Crypto TDS Examples (Simple Calculation)

Example 1: Selling Bitcoin

- Selling price: ₹1,00,000

- Crypto TDS (1%): ₹1,000

- Amount received: ₹99,000

Example 2: P2P Transaction

- Buying crypto worth ₹50,000

- Buyer deducts ₹500 as TDS

- Seller receives ₹49,500

Is Crypto TDS Adjustable Against Tax?

Yes. Crypto TDS can be adjusted against your final tax liability while filing your Income Tax Return (ITR).

- If your total tax liability is higher → TDS is adjusted

- If your total tax liability is lower → you may claim a refund

Penalty for Not Paying Crypto TDS

Non-compliance with crypto TDS rules can result in:

- Interest for late deduction

- Interest for late deposit

- Monetary penalties

- Legal consequences under the Income Tax Act

Timely deduction and deposit are crucial.

How to Check Crypto TDS Deducted?

You can verify deducted crypto TDS through:

- Form 26AS

- Annual Information Statement (AIS)

- Transaction reports from crypto exchanges

Always reconcile exchange data with Form 26AS before filing ITR.

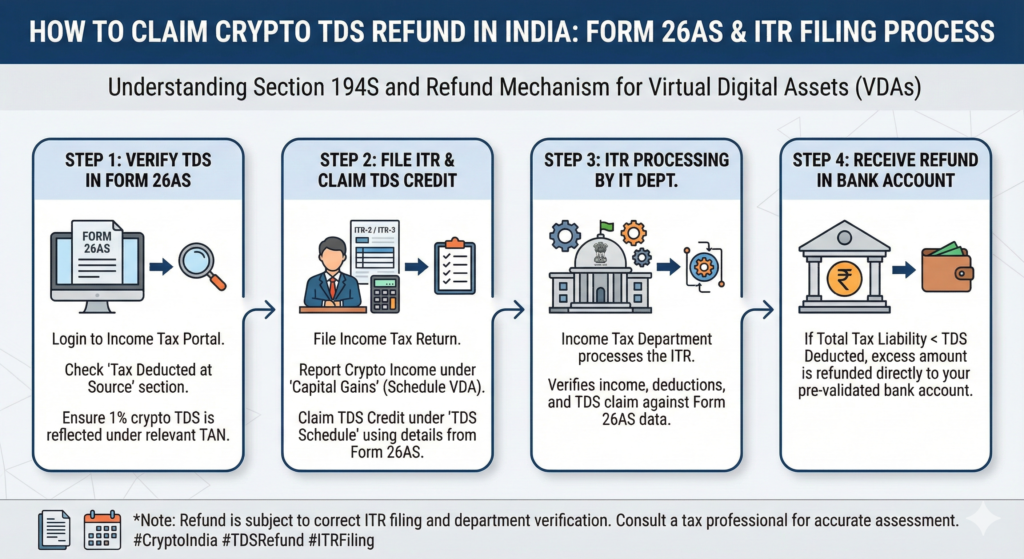

How to Claim Crypto TDS Refund in India?

If excess TDS has been deducted on your crypto transactions, you can claim a refund while filing your Income Tax Return (ITR). The deducted amount is reflected in Form 26AS and can be adjusted against your final tax liability.

- TDS deducted by exchange or buyer

- Reflected in Form 26AS

- Claimed while filing ITR

- Excess TDS refunded by Income Tax Department

Difference Between Crypto TDS and 30% Crypto Tax

| Crypto TDS | Crypto TAX |

| 1% | 30 % |

| Transaction-based | Profit-based |

| Adjustable | Final tax |

| Applies even in loss | Applies on gains |

Both apply independently.

Does Crypto TDS Apply Even in Loss?

Yes. Crypto TDS in India applies even if the transaction results in a loss. This is one of the biggest concerns for frequent traders, as it affects liquidity.

Latest Crypto TDS Updates for 2025

As of 2025:

- 1% crypto TDS remains unchanged

- No official reduction announced

- Government continues strict monitoring of crypto transactions

Any changes are expected only through future budget announcements.

How Crypto TDS Impacts Traders and Investors

- Reduced trading liquidity

- Higher compliance burden

- Increased record-keeping

- Stronger government oversight

Long-term investors are less affected compared to active traders.

Conclusion

Understanding crypto TDS in India is essential for anyone dealing in cryptocurrencies in 2025. While the 1% TDS rule increases compliance, proper planning and awareness can help you avoid penalties and manage taxes efficiently.

To understand the complete taxation framework, read our detailed guide on Crypto Tax in India (2025).

Recommended External Sources

Income Tax Department of India – https://www.incometax.gov.in

CBIC / Finance Act – https://www.cbic.gov.in

Is crypto TDS applicable on every transaction in India?

Yes, crypto TDS is applicable on almost every cryptocurrency transaction in India. Under Section 194S, a 1% TDS is deducted on the transfer of virtual digital assets, even if the transaction results in a loss.

Can crypto TDS be claimed as a refund?

Yes, crypto TDS can be adjusted against your final tax liability while filing your income tax return. If the total deducted TDS exceeds your tax payable, you may claim a refund.

Does crypto TDS apply to P2P transactions?

Yes, crypto TDS applies to peer-to-peer (P2P) crypto transactions. In such cases, the buyer is responsible for deducting and depositing the 1% TDS with the Income Tax Department.

Is crypto TDS applicable even if there is a loss?

Yes, crypto TDS in India applies even if the crypto transaction results in a loss. The 1% TDS is deducted on the total transaction value, not on the profit.